By signing up, you agree to our Terms of Use and Privacy Policy. We may use the info you submit to contact you and use data from third parties to personalize your experience.

Thank you for downloading!

CNC Machining

Tight tolerances and finishing capabilities, as fast as 2 days.

Sheet Metal

Experience the versatility & cost efficiency with flexible application options.

Injection Molding

Production-grade steel tooling, as fast as weeks.

Die Casting

Create high quality custom mechanicals with precision and accuracy.

3D Printing

FDM, SLS, SLA, PolyJet, MJF technologies.

Compression Molding

Experience lower tooling costs with high-quality durable parts.

Urethane Casting

Production quality parts without the tooling investment.

Our digital supply chain platform provides high-quality, scalable manufacturing solutions and is built to handle the full product lifecycle.

Learn moreJoin thousands of customers who trust Fictiv with their production programs.

Learn more2025 State of Manufacturing & Supply Chain Report

Download reportAirvine Scientific Success Story

The manufacturing behind Airvine's wireless Ethernet backbones.

Read case study

Insights from 300+ manufacturing and supply chain leaders—tracking the trends shaping 2026 and beyond.

I’m proud to present the 11th Annual State of Manufacturing & Supply Chain Report with MISUMI, underscoring our belief in an AI-powered digital future for manufacturing.

President and CEO, MISUMI Americas

AI adoption in manufacturing has reached a point of practical integration. This shift reflects a broader consensus that AI is now a required capability for maintaining competitiveness and operational reliability.

RYUSEI ONO

Representative Director & President

MISUMI Group Inc

It’s clear that implementing AI is critical for manufacturing and supply chain success.

Industry Director, Frost & Sullivan

Implementing AI into manufacturing and supply chain operations is vital to my company's future success.

97% of leaders are saying AI is already embedded in core workflows. The question is no longer if you use AI but how and to what extent.

NATE EVANS

Co-Founder & Head of Climate/AI, Fictiv

AI has advanced beyond experimentation or pilot projects—it’s now embedded in the daily workflows that run modern factories and supply chains.

Industry Director, Frost & Sullivan

As sourcing gets more complex and expensive to manage, we look for partners like Fictiv who simplify the process, reduce handoffs, and move faster. Digital manufacturing platforms have become essential to keeping our cycle times competitive.

DAVE EVANS

President and CEO, MISUMI Americas

Digital manufacturing platforms are becoming essential as manufacturers look to reduce complexity, improve engineering productivity, and optimize their supply chains.

RYUSEI ONO

Representative Director & President

MISUMI Group Inc

As sourcing gets more complex and expensive to manage, we look for partners like Fictiv who simplify the process, reduce handoffs, and move faster. Digital manufacturing platforms have become essential to keeping our cycle times competitive.

LILLIAN ORTIZ

Sr Project Manager, ITW Global Safety Monterrey

Sourcing is becoming more complex across the entire supply chain lifecycle, especially for custom and standard mechanical components. Having a single source for both significantly reduces that complexity.

DAVE EVANS

President & CEO, MISUMI Americas

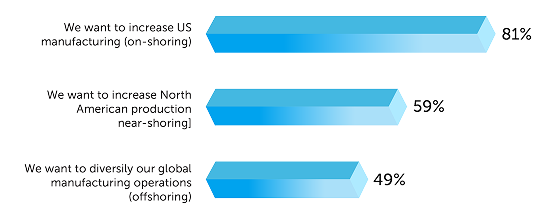

The rise of on-shoring manufacturing in North America is one of the most significant trends emerging in this report, but ensuring agility, capacity, and cost-effectiveness at scale still requires a globally connected supply chain.

ANDY SHERMAN

General Manager, Fictiv USA

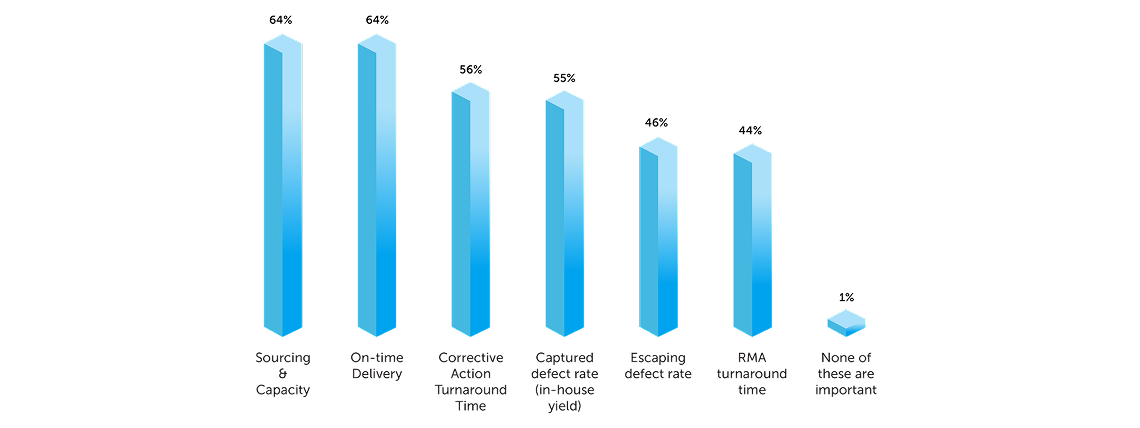

Supplier selection increasingly depends on supplier quality compliance, with documented systems replacing informal trust.

Industry Director, Frost & Sullivan

Sustainability has become a real operational mandate. As expectations rise, companies are aligning their sourcing practices with the kind of rigor outlined in Breakthrough Energy’s Five Grand Challenges—treating carbon, materials, and process impact as measurable criteria, not aspirations.

Nate EVANS

Co-Founder and Head of Climate/AI, Fictiv

The 2026 State of Manufacturing & Supply Chain reveals an industry undergoing a fundamental shift. Volatility—from geopolitics and tariffs to material costs—is no longer a temporary disruption but a permanent operating condition. At the same time, engineering capacity constraints and growing sourcing complexity are making it harder for companies to move fast and reliably. Manufacturing is being reshaped around a new set of realities, where speed, predictability, and resilience matter as much as cost.

In response, leaders are building supply chains around regional resilience, AI-enabled execution, and higher standards for quality, sustainability, and traceability. AI has moved from a “transformational” idea to essential infrastructure, powering faster decisions and more coordinated execution. The manufacturers that pull these capabilities into a cohesive operating system—combining regionalized networks, AI-driven workflows, and data-backed supplier performance—will set the competitive baseline in 2026, operating with greater confidence and durable advantages in cost, quality, and speed.

The 2026 State of Manufacturing findings are based on an online survey of 321 manufacturing leaders, covering topics such as AI adoption, supply chain disruption, new product innovation, operational efficiency, and sustainability. To enable year-over-year comparisons, select questions were repeated from the annual survey series (2020–2025), with an important caveat: trend comparisons from 2025 to 2026 are considered very reliable because the audience profile remained the same.

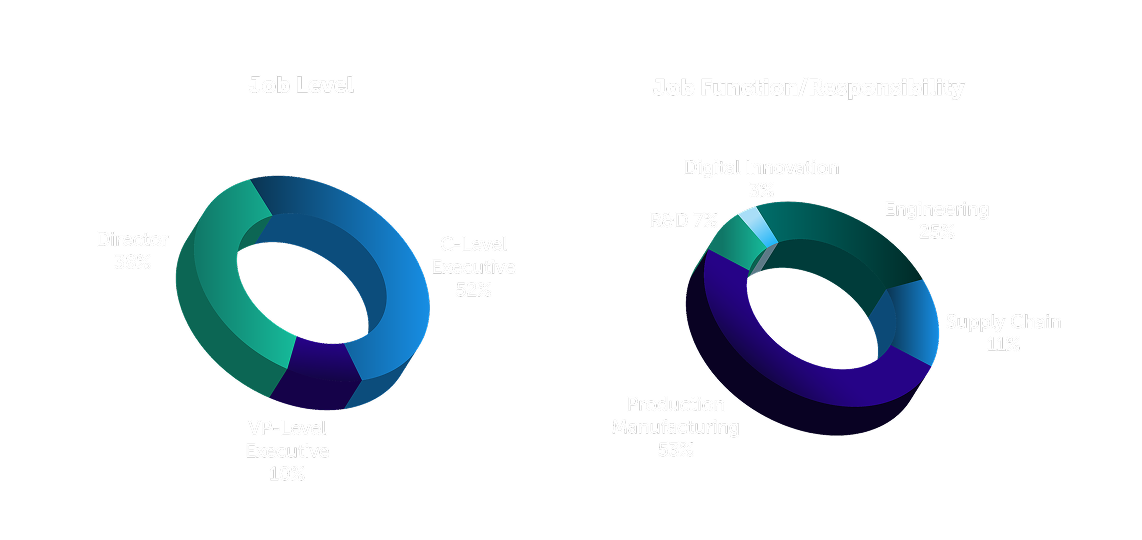

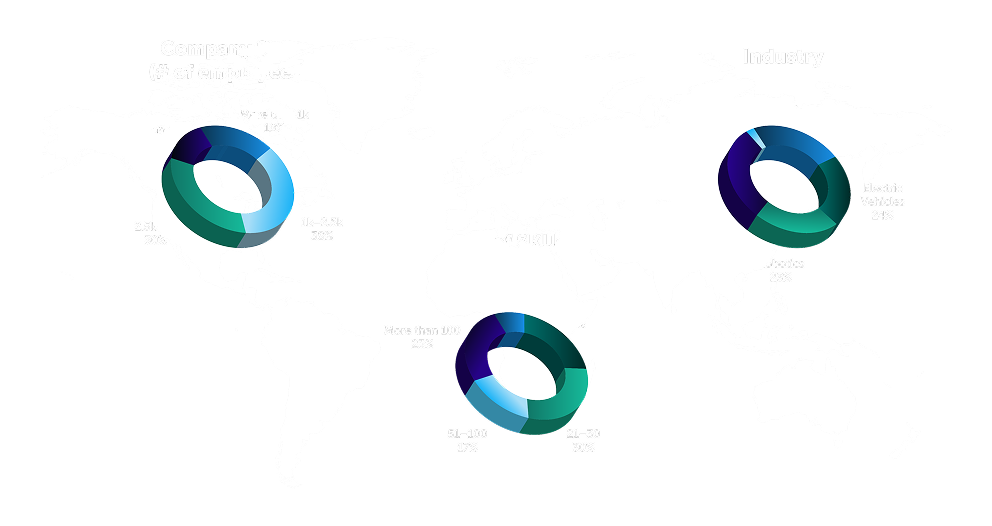

All qualified participants were director-level or above, spanning production manufacturing (53%), engineering (25%), supply chain (11%), R&D (7%), and digital innovation (3%)

Company representation leaned mid-to-large: 19% <1,000 employees, 38% 1,000–2,500, 30% 2,500–5,000, and 12%>5,000; respondents also spanned SKU complexity (7%: 2–5 SKUs; 23%: 6–20; 30%: 21–50; 17%: 51–100; 23%: >100). Industry mix was concentrated in priority verticals—MedTech (26%), Climate Tech (24%), EV (24%), Robotics (23%)—with “Other” minimal (2%, noted as including only Fictiv participants).